ARTICLE AD BOX

South Africa’s middle class is under a severe financial strain, with many struggling to find extra each month to cover instalments on vehicle and house loans.

Recent data from Eighty20’s Credit Stress Report for Q3 2022 showed that average monthly instalments for middle-class workers and other income segments have all seen a year-on-year increase, with the majority reaching around 7%.

Eighty20 created a National Segmentation (ENS) Customer Profiling Tool, which fuses credit bureau data with external data sets. Through statistical techniques, the company provides a comprehensive view of the finances of South African adults.

The group divided consumers across earnings and assets held, breaking datasets into middle-class workers, the mass credit market, “heavy hitters”, and comfortable retirees.

Middle-class workers represent the 4.1 million middle-income, credit-active population with families that have seen their average monthly instalments increase by 7% to R9,791.

When analysing the average instalments to monthly income ratio, there was a 9% year-on-year increase to 66%.

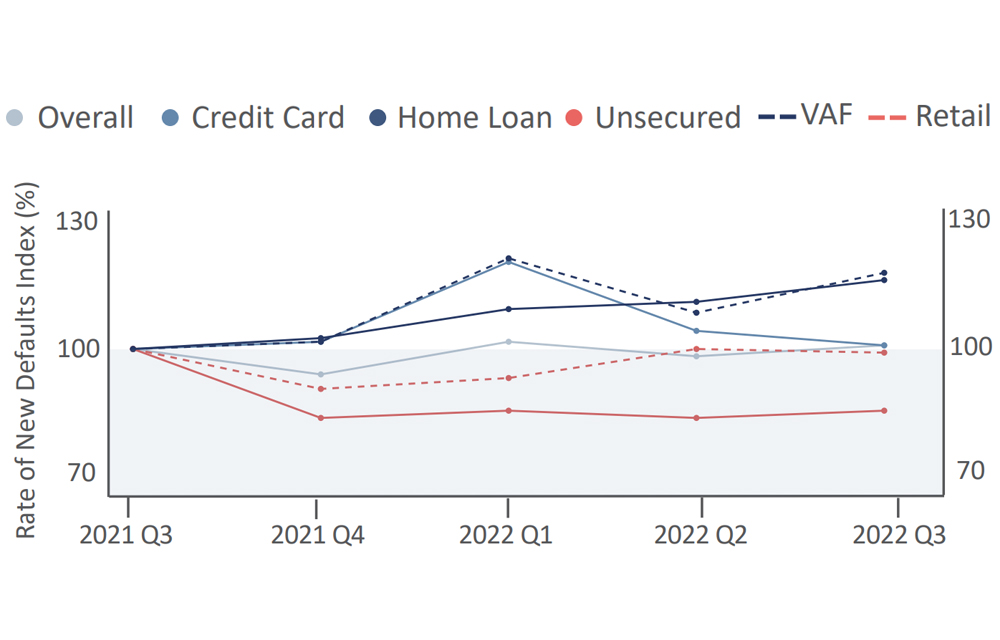

Of this category, 621,000 have a home loan, and 630,000 have vehicle asset financing. The report showed that there was also a 3% year-on-year decrease in the rate of new defaults, taking it down to 4.9%.

The report detailed that middle-class workers are feeling distressed most when it comes to instalments on cars and property.

“Their rate of new defaults on VAF loans went up by 21% YoY, with total VAF balances 55% of their home loan balances. The rate of new defaults on home loans went up 19% YoY with average instalments up 15% YoY,” reported Eighty20.

Eighty20 director Andrew Fulton told ENCA that a lot of financial pressure is a result of people taking out loans for big assets such as houses to cars during record-low interest rates in 2021 and then having to fork out more every month a year or so later due to rising interest rates.

Fulton provided the following example:

“If I had a 25-30-year-old daughter, I would have told her to buy a house and let’s say she bought R1.5 million in Cape Town. She would have bought that property, and a year later, she would have had to find more than R3,000 a month just to keep that property – just to pay those instalments on that one loan.”

He said that on top of that, she could also have a car loan to cover, which would be harder to pay off. If she was in the upper middle class, she might even have two car loans.

General credit overview

The report went on to detail that the current balance on all loans remained fairly flat over the third period of this year, at R2,231 billion – increasing by 1% (R17 billion).

Eighty20 showed that the overdue balance (loans over 30 days in arrears) had a significant decrease of R14 billion – a 7% drop over the quarter. “This decline was primarily driven by the closure of R9.8 billion overdue VAF balances more than nine months in arrears.”

“Loans in arrears decreased for the second quarter in a row, taking the total number in arrears to 18.4m (37.5% of all loans).”

“The largest decrease in loans in arrears was seen within those that are nine or more months in arrears, resulting in the percentage of all loans of this category decreasing by 0.6 percentage points quarter to quarter.”

According to Eighty20, there was an increase in the percentage of loans in good standing of 0.5%, indicating a potentially improving credit status for South Africans.

Read: Big turnaround for middle-class South Africans, says FNB

![]()

Another big stress for middle-class South Africans

English (US)

English (US)